September 11, 2023/FBNQuest

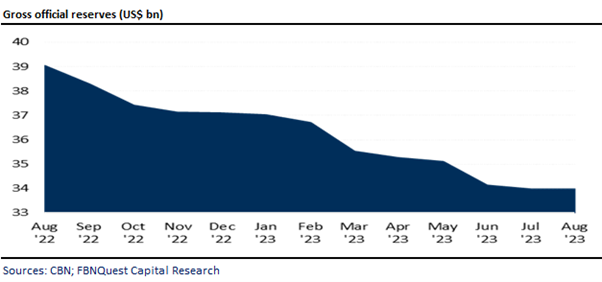

The CBN’s data shows that Nigeria’s gross official reserves increased marginally by around USD2m at the end of Aug ’23. The modest accretion is the first since Jul ’22, when the gross official reserves rose by USD64m. As shown by our chart, the trend has been downward. On average, the gross official reserves have declined by nearly -USD440m m/m since Aug ’22, and by -USD3.1bn year-to-date (ytd). The steady decline in gross official reserves, coupled with fx liquidity constraints has resulted in a weakening of investor confidence and a general loss of appetite by the offshore community.

Despite the CBN’s decision to float the naira in Jun ’23, it has had limited success in increasing foreign exchange inflows, as offshore investors have mostly remained cautious.

Monthly transactions on the investors’ and exporters’ (I&E) fx window for 8M 2023 are currently running at an average of USD2.1bn, compared with USD2.4bn over the comparable period of 2022.

At first glance, the total reserves as at end-Aug ’23 covered 7.0 months of merchandise imports on the basis of the balance of payments for the 12 months to Dec ’22 and 5.6 months when we add services.

However, the CBN’s recent publication of its audited accounts after a long period of non-disclosure, unveiled the possibility that the encumbered portion of the reserves may exceed initial estimates.

For instance, the 2022 accounts revealed a securitised loan of around USD7.5bn owed to JP Morgan and Goldman Sachs, as well as fx forwards of almost USD7bn.

We estimate that the CBN’s swap transactions with domestic banks amount to at least USD6bn.

The CBN has announced its commitment to clearing the FX backlog within two weeks. Although the exact mechanism remains undisclosed, what is clear is that domestic banks will have a significant role in this process.