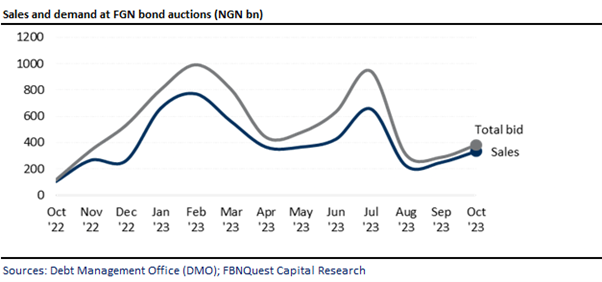

October 19, 2023/FBNQuest Research

At the primary auction of FGN bonds conducted by the Debt Management Office (DMO) on Monday, the agency offered its now regular offer size of NGN360bn worth of FGN paper to investors. While the agency fell slightly short of its sales target at NGN335bn, the outcome marked a significant improvement compared to the two preceding auctions. The sales-to-offer ratio reached 0.9x, a notable increase from the 0.7x and 0.6x recorded in Sept and Aug ’23, respectively. However, total subscriptions amounted to NGN383bn, representing a bid-to-cover ratio of 1.1x, slightly below 1.2x at the previous auction.

The direction of yields were upwards relative to the previous auction, and the trend indicated a conventional yield curve across the four instruments on offer.

The marginal rates for the 5-year (Apr ’29), 9-year (Jun ’33), 14-year (Jun ’38), and 29-year (Jun ’53) closed at 14.9%, 15.75%, 15.8%, and 16.6%, representing an average increase of 33bps relative to the previous auction.

Similar to the Sept ‘23 auction, investor demand was highest for the longest tenor on offer, or the 29-year June ’53 maturity, which was oversubscribed with a sales-to-offer ratio of 2.63x.

This compares with an average sales-to-offer ratio of 0.36x for the other three tenors on offer.

Despite the elevated yield environment, the increase in yields is outpaced by the significant rise in consumer prices, as underscored by the latest inflation print, which showed a 26.7% y/y rise in headline inflation for Sept ’23.

Year-to-date, the DMO has generated record sales of around NGN4.6trn through its monthly auction of FGN bonds. If non-competitive allotments are included, the figure rises to NGN5.1trn.

Despite the record-breaking amount, it is evident that the agency will fall short of meeting its domestic funding target of NGN7.0trn.

Going forward, we expect the MPC to keep a tight rein on monetary policy given the surge in domestic inflation, and the tight financial market conditions globally. As such, we continue to see yields elevated.