April 4, 2023/CSL Research

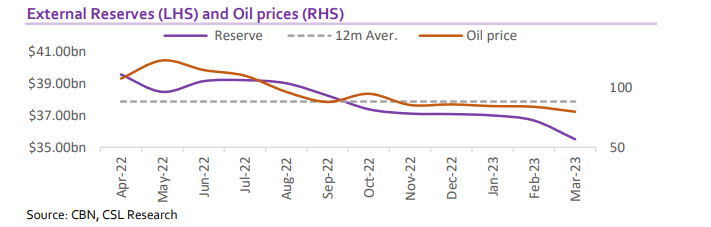

According to figures obtained from the CBN’s data on movement of external reserves, the country’s external reserves fell by US$1.60bn in Q1 2023. The figures show that external reserves fell to US$35.50bn as of 31 March 2023 from US$37.1bn as of 30 December 2022. Though other sources contribute to the country’s external reserves like foreign remittances and loans, the major source of inflow is crude oil sales receipt. In other words, gains in crude oil prices imply increase in the nation’s foreign exchange reserves. Oil prices trended up last year, given the impact of the Russia-Ukraine war on the global energy market butthe country failed to benefit from the high oil prices due to the drop in production numbers attributed to crude oil theft and decrepit oil infrastructure. Again, failure to eliminate subsidies implies subsidy payments grow with rising crude oil prices as landing cost of refined petroleum also increases. In 2023 however, crude oil prices started to moderate as the impact of the war began to wane.

Recent efforts by the CBN to boost the country’s external reserves have had little or no impact. The CBN had announced the RT200 FX programme to boost non-oil remittance into the reserve’s coffers. Precisely, the guideline stipulates that exporters will be paid N65.00 for every US$1.00 repatriated and sold at the Investors & Exporters Foreign Exchange (I&E) to Authorized Dealing Banks (ADBs) for other third-party use and N35.00 for every US$1.00 repatriated and sold at the I&E window for own use on eligible transactions only. The RT200 FX Program was unveiled in February 2022. The initiative was anchored on five pillars, namely: Value-adding Exports Facility, Non-oil Commodities Expansion Facility, Nonoil FX Rebate Scheme, Dedicated Non-oil Export Terminal, and Biannual Non-oil Exports.

At the end of last year, the World Bank asked the Central Bank to reconsider the RT-200 Programme despite the good intentions behind it. According to the World Bank, the program has created an additional foreign exchange window further worsening the nation’s FX problems. Exporters and their agents are alleged to be involved in a scheme where settle transactions are settled outside the I&E window at the parallel rate after benefiting from the RT-200 rebate, taking advantage of the wide parallel market premium and the CBN’s N65 and N35 per US$ incentives. Issues around the implementation program make us believe it may not be the solution to the country’s lingering FX scarcity. The parallel market premium remains wide despite over a year of the scheme’s introduction.

Click here to read full PDF copy of report